.svg)

Reports that the Securities and Exchange Commission (SEC) is preparing to repeal Rule 14a-8 would remove the federal framework underpinning shareholder proposals and turn its 2026 retreat from “no action” oversight into a full break with the process.

For Minerva, this is not just another proxy rule change. It is a test of whether shareholder proposal rights in the US can endure without the regulator that has long administered them, particularly given the absence of an equivalent foundation in company law.

The shift builds on last November’s decision to stop providing substantive “no action” guidance to issuers seeking to exclude proposals. A full repeal would go further, removing SEC involvement entirely and pushing disputes into courts and state jurisdictions.

For decades, both sides have relied on a federal administrative route that, despite criticism, offered a predictable way to test exclusions. Repeal would not end disputes, but it would move them into a more fragmented system.

Minerva CEO Sarah Wilson argued in March that shareholder proposal rights in the US are unusually fragile because they are not grounded in company law, as they are in most other developed markets. Instead, they depend on securities regulation.

That distinction is now central. Rights based on administrative practice can be narrowed or withdrawn without legislation. Without an equivalent governance function in company law, the role does not transfer. It disappears.

The significance therefore extends beyond proxy mechanics. It raises a broader question about the durability of shareholder rights in the world’s largest capital market.

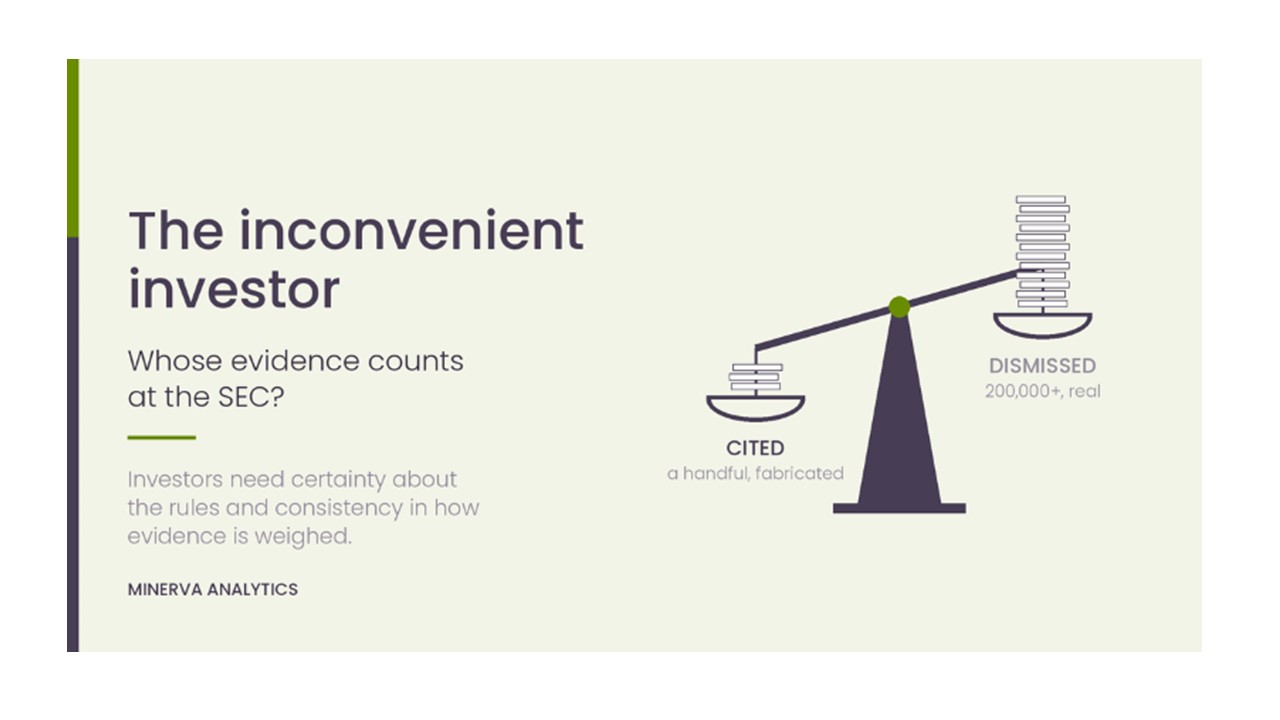

That issue is already being tested in court. In March, Interfaith Center on Corporate Responsibility and As You Sow challenged the SEC’s overhaul of the “no action” process, arguing it weakens scrutiny and limits proponents’ ability to respond.

Some companies have faced legal challenges over exclusion decisions, while others have taken a more cautious approach by including proposals they might previously have contested.

A successful challenge could restore substantive review in the near term. But if the SEC proceeds with repeal, litigation would only revive the current process temporarily rather than resolve its underlying vulnerability.

Chair Paul Atkins has argued that the SEC should not opine on matters that belong to state corporate law, and that the current system allows investors with small holdings to drive engagement on issues beyond core business concerns. Resource constraints have reinforced that position.

But the argument cuts both ways. If proposal oversight is treated as outside the SEC’s remit, and company law does not fill the gap, a governance mechanism investors have treated as durable may prove contingent.

A formal SEC proposal is expected later this year, with input from investors and business groups likely to shape the outcome. The immediate question is how workable the system remains through the next proxy cycles. The more important one is whether shareholder proposal rights can remain a reliable feature of US markets if Rule 14a-8 is removed.

If Rule 14a-8 disappears, the issue is no longer how proposals are reviewed, but whether the mechanism survives at all.

-1.avif)