.svg)

15 October 2021

Alex Whitebrook

October 15, 2021

In a second blog post in our series on Australia’s upcoming AGM season, Minerva provides an overview of the remuneration strike system and identifies key remuneration votes to look out for in 2021. This blog article is based on analysis from Minerva’s upcoming Australia Peak Season Preview briefing – say hello@minerva.info for more information.

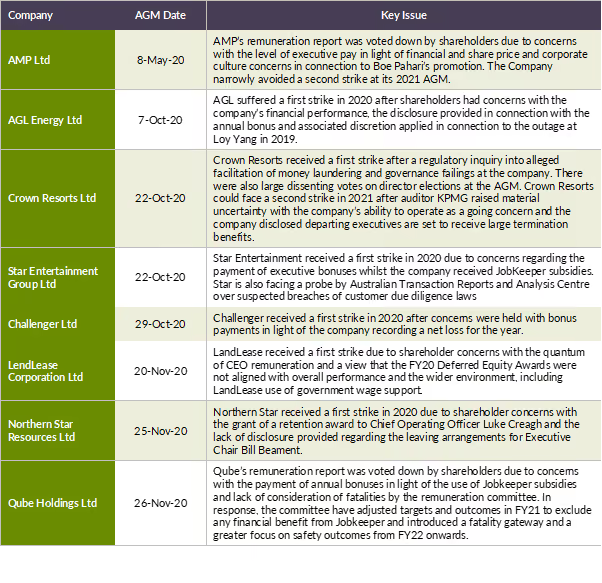

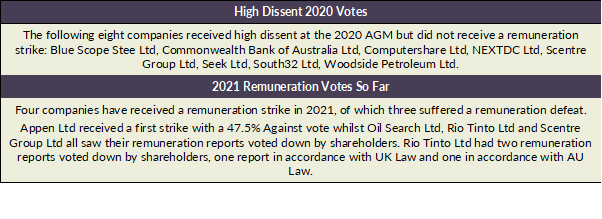

The early months of 2021 indicate shareholders could be taking a more active stance on voting on remuneration reports, with three companies in the ASX100 having their remuneration reports already voted down – more than the two voted down in the whole of 2020 and zero in 2019.

In 2020, eight companies in the ASX100 received a remuneration strike and will place a ‘board spill’ resolution on the 2021 AGM agenda in the event of a second strike (see details of the 'two strike rule' below). A further eight companies received dissent of at least 20% but less than 25% ‘Against’ votes. Shareholders will want to pay attention to how the boards have responded to shareholder concerns:

The two-strikes rule was introduced in 2011. Under the rule, if shareholders vote against a company’s executive remuneration report two years in a row, the board may be voted out of office via a ‘board spill’ resolution. The intention behind the strike system is to encourage greater transparency and engagement on executive remuneration as well as greater director accountability where boards are unresponsiveness to shareholder concerns.

A ‘first strike’ occurs when a company’s remuneration report receives an ‘against’ vote of 25% or more. The ‘second strike’ occurs when a company’s subsequent remuneration report also receives ‘against’ votes of 25% or more.

When a second strike occurs, the shareholders will vote at the same AGM on a ‘board spill’ resolution which if passed, the company is required to hold a spill meeting within 90 days at which all individuals who were directors when the directors’ report was considered at the most recent AGM will be required to stand for re-election (other than the managing director). However, shareholders rarely, if ever, vote through the board spill resolution – this suggests the system may have limited effectiveness in dealing with unresponsive boards as shareholders may wish to avoid destabilising the board over remuneration concerns.

It should be noted that only ‘for’ and ‘against’ votes are considered when determining whether a strike has occurred, and abstentions are not included in the calculations. Whilst abstentions are not counted, many investors positively abstain to indicate their lack of support for management. Using a sporting metaphor, a positive abstain is a “Yellow Card” to send a warning to management or as part of an engagement escalation strategy. However, the exclusion of abstentions in determining whether a strike has occurred demonstrates the potential pitfalls of abstaining when concerns are held.

.avif)

-1.avif)